The Medical Office Building Market: Trends Both Past and Present

Medical office buildings are an often overlooked asset because most real estate investors simply do not understand the nuances of this property type. A little homework helps to demystify these buildings and in doing so, investors will find that medical office space can be a terrific, stable, income-producing addition to their portfolios.

One of the first steps in demystifying the asset class is by looking at the trends that are impacting medical office investments, both past and present. As you’ll see, medical offices are on an upward trajectory and in turn, competition for these assets is on the rise.

Related: Investors Must Think for Themselves

Investment Activity

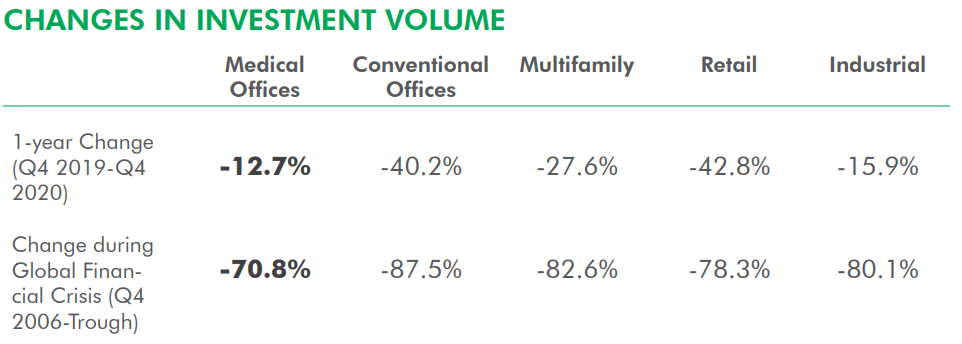

Transaction volume and investment activity are strong indicators about the prospects of any real estate asset class. During the depths of the COVID crisis, MOB annual investment volume declined by 12.7%, according to Real Capital Analytics. On the surface, this may seem high, but it is lower than any other major property type. During this same time, conventional office was down 40.2%, multifamily investment volume dropped 27.6%, retail declined 42.8% and industrial investment slipped by 15.9%.

Source: Real Capital Analytics, February 2021. Based on independent reports of properties and portfolios $2.5 million and greater. Note: Based on four-quarter sum of transactions. https://www.rcanalytics.com/tag/medical-office/

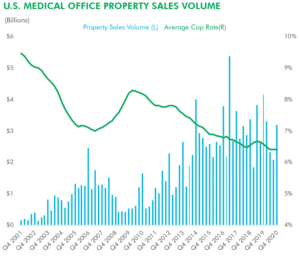

Moreover, in Q4 2020, the average price per square foot of medical office transactions was 3.7% higher than in Q4 2019, which proves that medical office is resilient even in the wake of widespread economic turmoil.

Investors, particularly institutional investors, are taking note. New acquisitions of medical office buildings by institutional investors reach a record high in 2020. Individual investors are following suit. According to the 2021 Emerging Trends in Real Estate survey by PwC and the Urban Land Institute, real estate investors are calling medical office one of the “expected best bets in 2021”.

Vacancies

Another reason why real estate investors are bullish about medical office is because of its low vacancy rate compared to traditional office. According to Colliers, office vacancies were at 12.6% in mid-2020 vs. just 8.6% for medical office buildings. Even during the Great Recession when medical office vacancies were at their highest, MOB vacancies never exceeded 10.4%.

Rent Growth

Despite the pandemic, rent collections among MOB tenants remained strong. According to a survey of medical office landlords, collection rates averaged 95% even during the depths of the pandemic. This shows that despite economic swings, medical office rents are reliable.

According to CoStar, a commercial real estate database, MOB asking rents average around $22.30 per square foot (NNN). Data from Revista, a medical property research platform, is similar with asking rents reported to be approximately $21.40 per square foot (NNN) for the properties in its database. Some regions, like New York and Los Angeles, have higher asking rents but these areas also have lower vacancy rates.

Asking rents have remained relatively steady over the past six to eight years, never fluctuating by more than +/- $4 per square foot on average. In other words, medical office rents do not experience the same peaks and valleys that other asset class rents are prone to. Rents remained in this range even during the Great Recession (compared to traditional office rents which decreased by nearly 15% during the 2008-2010 recession).

Moreover, rents are now on the rise. Revista notes that rents are steadily increasing by 2-3% per year. In 2020, the average price per square foot rent for MOB buildings increased by a more substantial 5.5%, a factor attributed to limited supply. Rent increases are expected to be more profound at new, purpose-built MOB facilities due to skyrocketing construction costs.

Cap Rates

Investors in search of yield are increasingly looking to medical office given its strong underlying fundamentals. However, increased investor demand and limited asset availability is causing cap rates to compress. According to CBRE data, the average cap rate on sales of MOB facilities compressed by about 20 basis points year-over-year in 2020, with the average cap rate for portfolio sales declining by 100 basis points to about 5.52%. The average cap rate for individual MOB sales dropped to 6.61% during this same time (dipping below the previous record lows of 6.7% in Q3 2016). For the first time, medical office cap rates are now lower than traditional suburban office cap rates which is indicative of growing investor demand and optimism about the sector. In the Sun Belt region, where population growth among older Americans is driving MOB demand to new highs, cap rates average about 60 basis points lower than the national average.

Source: CBRE US Research, Medical Office Trends 2021: https://www.cbre.us/research-and-reports/US-Medical-Office-Trends-2021

Despite the compression of cap rates, medical office cap rates are still higher than multifamily cap rates which are hovering in the low 5% range nationally. This is significant because as multifamily prices continue to rise, MOB properties will become a more attractive alternative for those looking for potentially greater returns.

Construction

Construction of new medical office buildings tends to lag the construction of other property types, in large part because these facilities are expensive to build and often require purpose-built facilities. This is especially true when leasing to hospital-affiliated tenants. To put these costs in perspective, medical office buildings cost an average of $498 per square foot to build compared to distribution centers ($214/SF), strip malls ($245/SF), and traditional suburban office ($313/SF).

Therefore, MOB developers tend to be highly disciplined and do not build “on spec”; instead, they work to create an ecosystem of healthcare tenants that compliment one another (e.g., dentists, physicians, physical therapists and other specialty care providers). Location decisions are highly data-driven based on demographics, population density and rates of insurance coverage, which all influence where to expand and how many physicians will be needed in a local market.

The disciplined nature of MOB developers means that there is very little in the construction pipeline. The amount of space currently under construction nationwide totals less than 1% of the existing MOB stock. Atlanta and Chicago are tied for the greatest amount of medical office space under construction among the top ten metro areas, with both at 1.7 million square feet under construction. New York follows with 1.6 MSF. Some markets, like Philadelphia, have less than 500,000 SF of development in the pipeline.

MOB space under construction as a share of inventory is highest in Atlanta at 6.1%, followed by Miami at 5.9% and Washington, DC at 5.2%.

This lack of new construction is helping to keep vacancies of existing facilities low and is driving MOB rents to all-time highs.

Are you an investor? Our professional team continually analyzes the market for excellent opportunities. We can package something to fit your specific financial situation. Contact Alliance today to learn more.

Absorption Rates

Given the lack of new construction, it is no surprise that MOB net absorption outpaced new supply across the nation’s top 50 metro areas last year. Nationally, there was 15.3 million square feet of net absorption in 2020 with just 13.7 million square feet of space delivered.

In fact, MOB absorption rates have outpaced completions of new supply every year since 2010, driving steady decreases in the national vacancy rate.

Absorption rates are especially high in the Sun Belt region where robust population growth is driving demand for medical office space. Houston, Tampa, Phoenix, and South Florida have among the highest net absorption rates. Not only do these markets have strong absorption levels, but they are also among the top markets for absorption as a percentage of net existing rentable area (NRA), with Tampa highest among all markets at nearly 6%.

Subscribe to our commercial real estate newsletter.

Building Conversions

Given growing demand for medical office space and a lack of new construction, many real estate developers are starting to convert traditional office space into medical office. Another prominent trend is the conversion of vacant retail stores into medical office properties. This last trend is especially significant.

Increasingly, MOBs are opening on retail pad sites located at larger mixed-use projects. Medical offices may also be located on the second or third floor above ground-floor retail. By co-locating in a more traditional retail environment, healthcare providers gain greater visibility, better access, and branding opportunities that give them a competitive advantage over those located in more isolated suburban office parks. Medical office tenants appreciate the proximity to other retail anchors like grocery stores and pharmacies, local neighborhood services that already draw their target demographic. It also opens the door to physicians looking to support their operations through on-site retail, such as dermatologists that sell their own private label skincare products or endoscopists who sell weight-loss programs.

MOB facilities located in retail environments are also attractive to patients and staff. One of the biggest complaints patients usually have about healthcare visits is long wait times. Moving forward, it’s not unthinkable to have medical providers give patients “pagers” like they would get at a restaurant, which would allow patients to go run errands or do other shopping on-site while remaining close by.

Similarly, as competition for skilled healthcare workers increases, facilities located in a retail environment may find it easier to attract and retain staff. Staff, who might otherwise be confined to an isolated office park, will be drawn to the convenience that retail environments offer as they can more easily pop out for lunch or to run errands on their breaks.

For all of these reasons, investors will find healthcare providers increasingly willing to pay a premium to locate in desirable retail environments.

Employment Growth

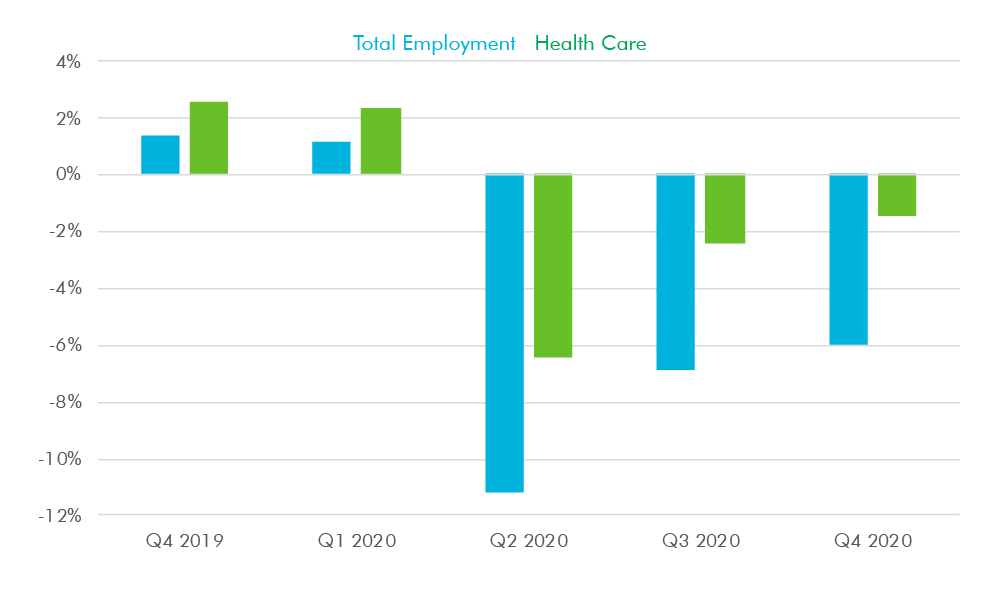

The healthcare sector is one of the labor market’s most stable industries. According to a recent CBRE analysis, although healthcare employment experienced a pandemic-induced dropoff in 2020, the decline (6.4% year-over-year) was much lower than employment losses for the broader economy (11.2%). The decline in healthcare employment was a result of some patients pausing treatments and rescheduling routine visits during the depths of the pandemic. Those patents are now lining up for visits, which has created a backlog of demand for healthcare services. In turn, healthcare employment has bounced back in short order. Employment has been increasing since mid-2020 and by Q4 2020, was down only 1.5% year-over-year compared to 6.0% for the labor market as a whole.

Source: CBRE US Research, Medical Office Trends 2021: https://www.cbre.us/research-and-reports/US-Medical-Office-Trends-2021

The pandemic aside, healthcare occupations are expected to be in high demand for years to come. According to the U.S. Bureau of Labor Statistics, employment in healthcare occupations is expected to grow 16% between 2020 and 2030, much faster than the average for all occupations, adding about 2.6 million new jobs. In fact, healthcare occupations are projected to add more jobs than any other sector – something the BLS attributes to the nation’s aging population and growing demand for healthcare services.

Related: Are You Investing Enough for Retirement?

Final Thoughts on the Medical Office Building Market Trends

By all indications, medical office is a resilient sector and as proven during both the Great Recession and pandemic, can weather economic downturns better than other property types.

The sector’s resiliency, as well as strong underlying fundamentals, has increased investor appetite for healthcare-related real estate. And as investor appetite has grown, medical office buildings have emerged as the most popular property type within the niche. Given the trends outlined above, it’s no wonder why. As yields for traditional real estate asset classes compress, we expect to see more investors – institutional and retail investors alike – pour capital into the medical office sector in search of higher yield and a relatively safe investment alternative.

Are you considering commercial real estate investments? Our portfolio includes medical, industrial, retail, and office properties, with deals ranging from $1M to $25M. Visit Alliance to learn more.

POSTED BY

Ben Reinberg

Founder & CEO | Alliance Group Companies

Ben Reinberg is Alliance Group Companies' founder and CEO.

Since 1995, Alliance Consolidated Group has acquired and invested in medical properties with net leases between $3 and $25 million across the United States. With decades of commercial real estate experience, we take pride in committing to meeting the goals of our Sellers, as we consistently and seamlessly adhere to successful closings.